US Reshoring - Executive Summary

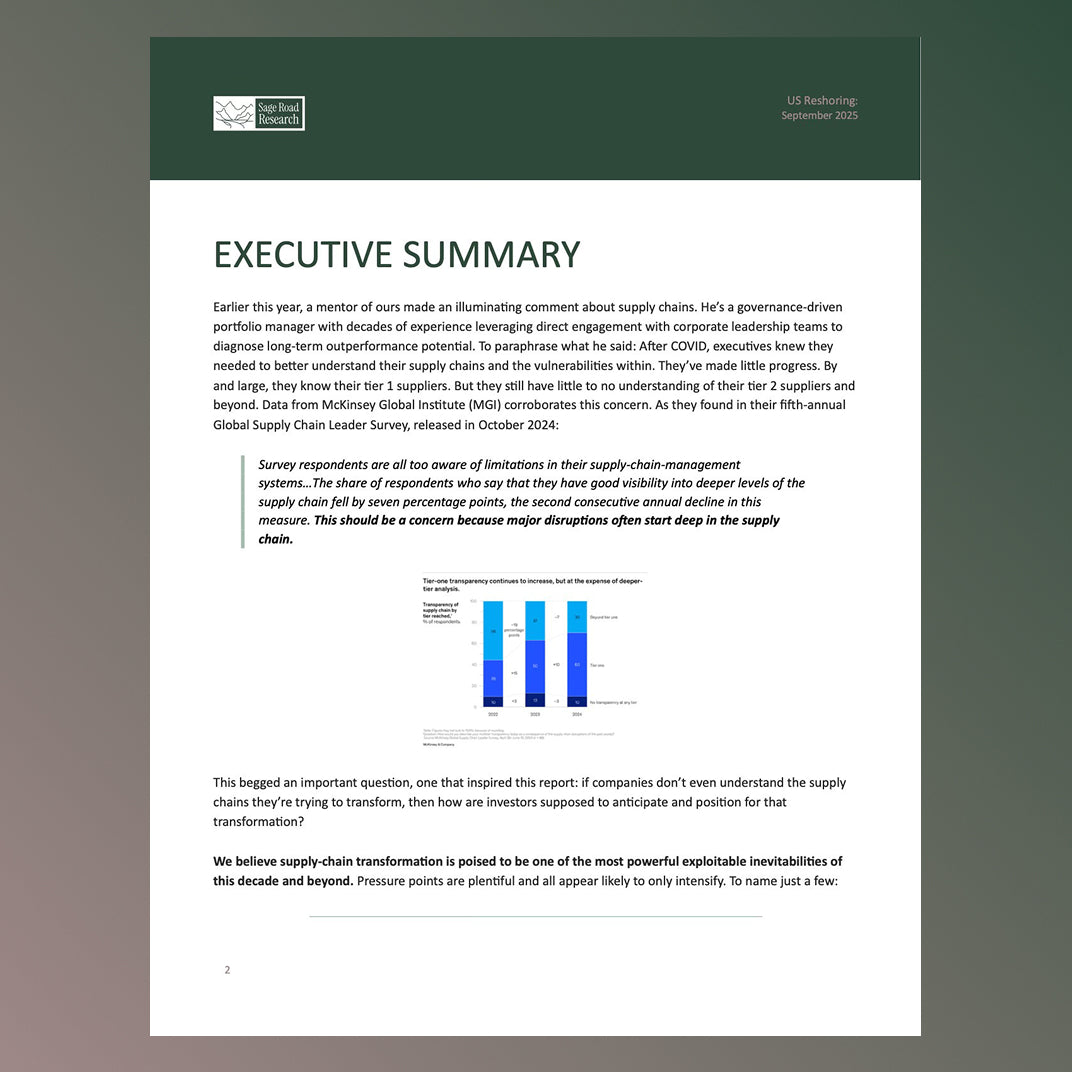

Earlier this year, a mentor of ours made an illuminating comment about supply chains. He’s a governance-driven portfolio manager with decades of experience leveraging direct engagement with corporate leadership teams to diagnose long-term outperformance potential. To paraphrase what he said: After COVID, executives knew they needed to better understand their supply chains and the vulnerabilities within. They’ve made little progress. By and large, they know their tier 1 suppliers. But they still have little to no understanding of their tier 2 suppliers and beyond. Data from McKinsey Global Institute (MGI) corroborates this concern. As they found in their fifth-annual Global Supply Chain Leader Survey, released in October 2024:

Survey respondents are all too aware of limitations in their supply-chain-management systems…The share of respondents who say that they have good visibility into deeper levels of the supply chain fell by seven percentage points, the second consecutive annual decline in this measure. This should be a concern because major disruptions often start deep in the supply chain.

This begged an important question, one that inspired this report: if companies don’t even understand the supply chains they’re trying to transform, then how are investors supposed to anticipate and position for that transformation?

We believe supply-chain transformation is poised to be one of the most powerful exploitable inevitabilities of this decade and beyond. Pressure points are plentiful and all appear likely to only intensify. To name just a few: Wages are rising in emerging markets, compromising the cost/benefit equation of today’s globalized supply-chain status quo. China alone has seen average salaries more than double over the last decade. Meanwhile, geopolitical instability and climate change threaten a higher rate of supply-chain disruption. Today, 92 countries are engaged in conflicts beyond their borders, the highest number since WWII, according to the Global Peace Index. And the globe suffered 58 $1 billion-plus natural disasters in 2024 after suffering 73 in 2023, according to Gallagher Re.

On average, companies across sectors can now expect to suffer a supply-chain disruption lasting one to two months every 3.7 years with a financial fallout equivalent to 30% of one year’s EBITDA, according to MGI calculations. In the months and years to come, supply-chain transformation will be a focus of Sage Road Research. We intend to provide our clients with a holistic roadmap for investing in supply-chain transformation, dissecting the theme across all actionable global facets.

From great complexity, technological disruption, and political and cultural divisiveness will come both alpha opportunity and downside risk. We believe deep research will prove the essential edge in pinpointing winners and losers across asset classes, regions, and sectors. For this report, we’ll begin with US reshoring. Our topline conviction: the US is likely to reshore more and faster than the market and even many corporate leaders anticipate, instigated by politics, but even more so, by the AI revolution.

The US is now in the midst of its third-consecutive presidential administration for which reshoring is a tentpole policy priority—Trump 1.0 to Biden to Trump 2.0. Roughly 47% of the US population believes that the US has suffered due to globalization and roughly 80% believes that outsourcing of jobs to other countries has hurt American workers, according to Pew Research. Corporate leaders increasingly recognize reshoring as an imperative. Reshoring investment is surging: In 2023, US reshoring announcements totaled $933 billion. By the end of 2024, that figure reached $1.7 trillion, according to Eaton. And the growth appears poised to continue. As Bain found in a 2024 survey, 81% of 166 CEO and COO respondents had plans to bring supply chains closer to market, an increase of 18 percentage points since 2022.

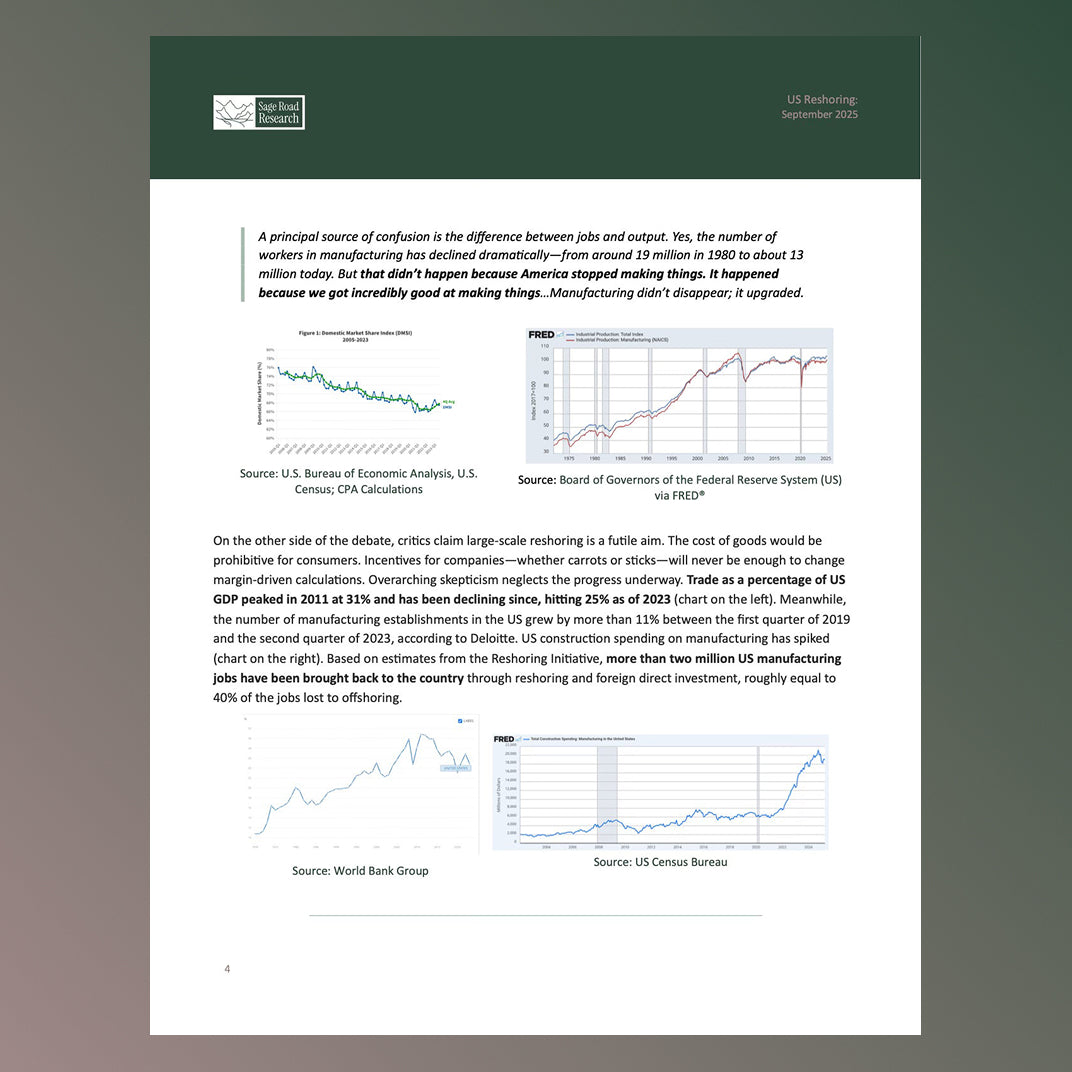

Political polarization has contributed to widely repeated hyperbole on both sides of the reshoring debate. Advocates of urgent reshoring blame globalization for crippling US manufacturing and hollowing out communities across the country. This is only partly true. US manufacturing production has fallen but still met 67.5% of domestic demand in 2023 (chart on the left). Meanwhile, inflation-adjusted manufacturing output in the US is near all-time highs, up 177% since 1975 (chart on the right). As Veronique de Rugy, a senior research fellow at the Mercatus Center at George Mason University, wrote in a Los Angeles Times op-ed in March:

A principal source of confusion is the difference between jobs and output. Yes, the number of workers in manufacturing has declined dramatically—from around 19 million in 1980 to about 13 million today. But that didn’t happen because America stopped making things. It happened because we got incredibly good at making things…Manufacturing didn’t disappear; it upgraded.

|

Source: U.S. Bureau of Economic Analysis, U.S. Census; CPA Calculations |

Source: Board of Governors of the Federal Reserve System (US) via FRED® |

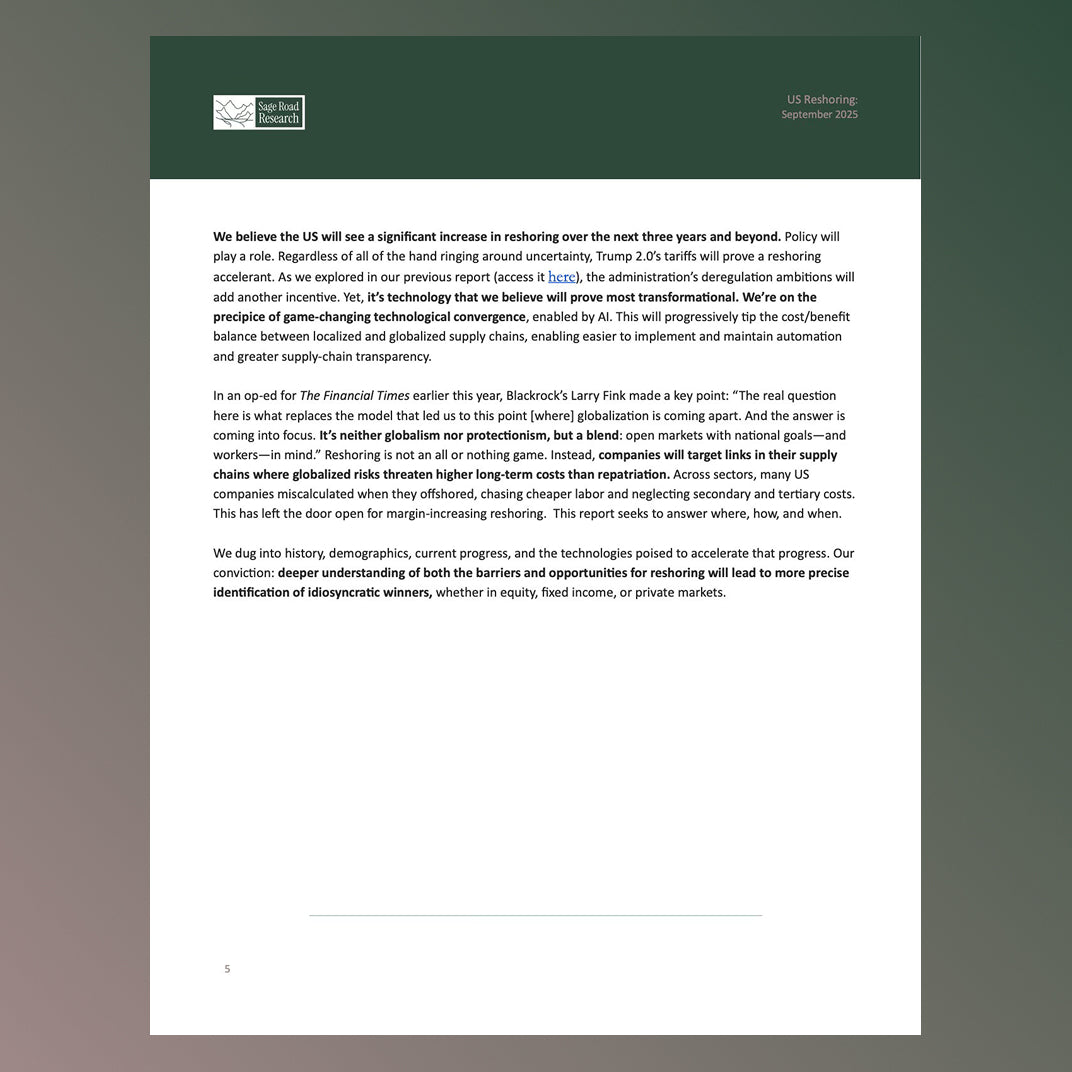

On the other side of the debate, critics claim large-scale reshoring is a futile aim. The cost of goods would be prohibitive for consumers. Incentives for companies—whether carrots or sticks—will never be enough to change margin-driven calculations. Overarching skepticism neglects the progress underway. Trade as a percentage of US GDP peaked in 2011 at 31% and has been declining since, hitting 25% as of 2023 (chart on the left). Meanwhile, the number of manufacturing establishments in the US grew by more than 11% between the first quarter of 2019 and the second quarter of 2023, according to Deloitte. US construction spending on manufacturing has spiked (chart on the right). Based on estimates from the Reshoring Initiative, more than two million US manufacturing jobs have been brought back to the country through reshoring and foreign direct investment, roughly equal to 40% of the jobs lost to offshoring.

|

Source: World Bank Group |

Source: US Census Bureau |

We believe the US will see a significant increase in reshoring over the next three years and beyond. Policy will play a role. Regardless of all of the hand ringing around uncertainty, Trump 2.0’s tariffs will prove a reshoring accelerant. As we explored in our previous report (access it here), the administration’s deregulation ambitions will add another incentive. Yet, it’s technology that we believe will prove most transformational. We’re on the precipice of game-changing technological convergence, enabled by AI. This will progressively tip the cost/benefit balance between localized and globalized supply chains, enabling easier to implement and maintain automation and greater supply-chain transparency.

In an op-ed for The Financial Times earlier this year, Blackrock’s Larry Fink made a key point: “The real question here is what replaces the model that led us to this point [where] globalization is coming apart. And the answer is coming into focus. It’s neither globalism nor protectionism, but a blend: open markets with national goals—and workers—in mind.” Reshoring is not an all or nothing game. Instead, companies will target links in their supply chains where globalized risks threaten higher long-term costs than repatriation. Across sectors, many US companies miscalculated when they offshored, chasing cheaper labor and neglecting secondary and tertiary costs. This has left the door open for margin-increasing reshoring. This report seeks to answer where, how, and when.

We dug into history, demographics, current progress, and the technologies poised to accelerate that progress. Our conviction: deeper understanding of both the barriers and opportunities for reshoring will lead to more precise identification of idiosyncratic winners, whether in equity, fixed income, or private markets.